Credit Card

A credit card is a payment card made of plastic or metal, issued by banks, allowing users to purchase goods and services from merchants that accept card payments. It represents a line of credit that can be used without incurring interest if repaid within a specified period. However, if users exceed this period, interest charges apply. Additionally, credit cards often come with joining and renewal fees.

Credit card determines the credit limit through a process called underwriting, which includes financial factors like:

- Credit score

- Payment history

- Income Level

- Credit Utilization

- Monthly expenses

What are the uses of credit cards?

What documents are required for a credit card?

What are the Advantages and Disadvantages of using a credit card?

What are the eligibility criteria for credit cards?

What are the required documents for a Credit Card?

How Credit card limit is determined?

Terms used in Credit Card Billing System

1) Statement date or billing date

The credit card statement date marks the end of a monthly period, summarizing all expenses made during that time. It includes details of the previous month’s payments, the total repayment due, and the deadline for paying the full amount to avoid any charges or fees. On the statement date, the bank sends you an email, allowing you to choose whether to pay the minimum amount or the full balance.

2) Due Date

The due date follows the statement date, typically falling 15 to 20 days later, also known as the grace period for paying off your bills. If you pay the full amount by the due date, you avoid interest charges. However, if you miss the due date, you will incur significant interest charges and your credit score may decline.

3) Minimum Amount Due:

The minimum due amount is a percentage of the total outstanding balance that you must pay to the bank by each bill date. This percentage varies by bank but typically ranges between 10% and 100% of the total balance. Interest is charged on the remaining unpaid amount.

Credit Card

- Uses of Credit Card

- What documents are required for credit card?

- Steps for Credit Card

- Eligibility For Credit Card

- What are the required documents For Credit Card?

- How Credit card limit is determined?

- Credit Card Billing Cycle

- Terms used in Credit Card Billing System

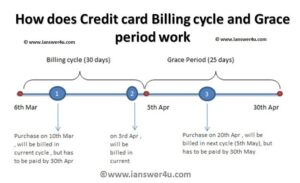

- Example of Credit Card Billing Cycle

- Credit Card in Nepal

- Total Number of Credit card Issued and Total Transaction Amount

- Fees and Charges of Credit Card

- Disadvantage of Using Credit Card

- How Credit Card Laundering Works